TL;DR:

- Financial institutions that treat customer experience as a core business function see faster growth and multimillion-dollar revenue gains.

- Effective CX links loyalty, compliance, and personalization, reducing churn and regulatory risks simultaneously.

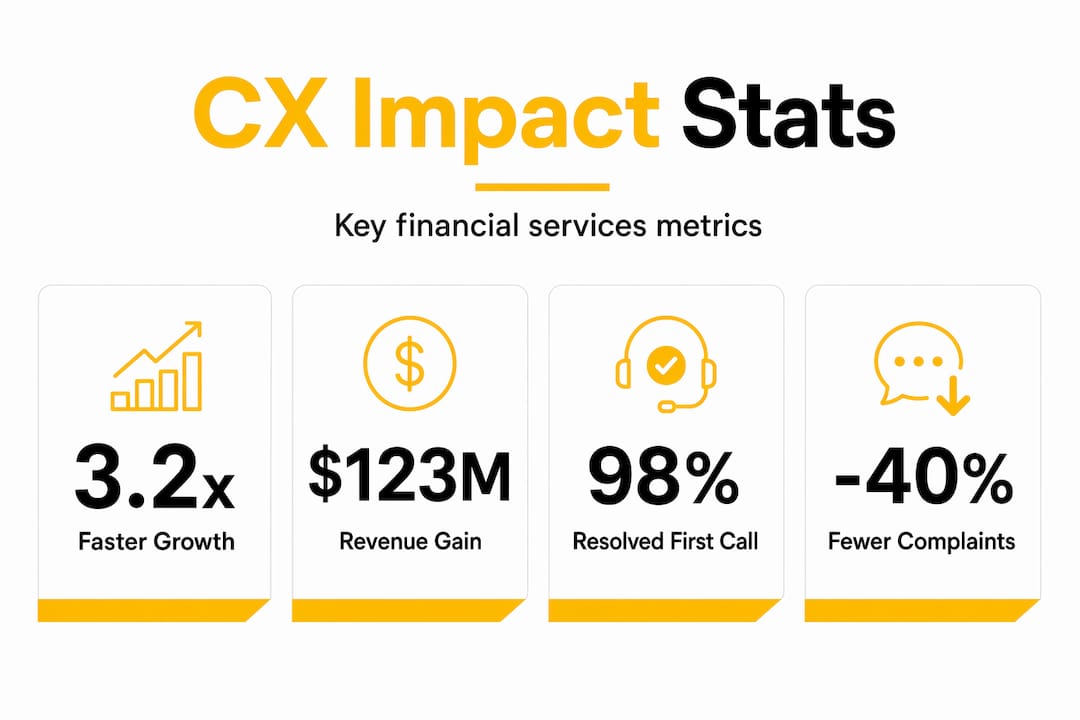

Financial institutions that treat customer experience as a marketing function are leaving serious money on the table. The role of CX in financial services has evolved far beyond satisfaction scores and call center scripts. It now sits at the center of growth strategy, compliance management, and long-term loyalty. Banks with optimized CX grow 3.2x faster than their competitors and generate $123 million in incremental revenue per one-point CX Index improvement. That is not a marketing outcome. That is a business mandate.

Table of Contents

- Key takeaways

- The role of CX in financial services, defined

- How CX drives growth, loyalty, and compliance

- Common CX pitfalls in financial services

- Practical CX strategies for financial services executives

- Measuring and sustaining CX success

- What I’ve learned about CX in financial services after years in the field

- How Altiamcx helps financial services organizations build better CX

- FAQ

Key takeaways

| Point | Details |

|---|---|

| CX drives measurable revenue | A one-point CX Index improvement can generate $123M in incremental revenue for multichannel banks. |

| Compliance and CX must integrate | Embedding compliance into CX design turns regulatory constraints into competitive differentiation. |

| Channel handoffs destroy loyalty | Customers who repeat information across channels churn at significantly higher rates than those who do not. |

| Complaints signal systemic risk | Sustained complaint growth predicts regulatory enforcement before formal actions occur. |

| Measurement requires multiple signals | NPS trend direction, customer effort scores, and complaint data together tell a more accurate story than any single metric. |

The role of CX in financial services, defined

Customer experience in finance is not a department. It is the sum of every interaction a customer has with your institution, from the moment they open an account to the day they file a complaint or renew a product. That scope matters because most executives still mentally file CX under “customer service” or “marketing,” which creates dangerous blind spots.

In reality, CX in financial services operates across four distinct touchpoint categories:

- Digital channels: Mobile apps, online banking portals, and automated chat workflows that now handle the majority of routine transactions. Digital banking adoption sits at 82%, with 45% of all transactions happening exclusively via mobile.

- Branch and in-person interactions: High-stakes moments like loan consultations, dispute resolution, and financial planning conversations that still demand human judgment and empathy.

- Contact centers: The frontline for complaints, complex queries, and escalations. Only 34% of complaints are resolved on first contact in banking, which is a significant operational gap.

- Back-office and operational processes: Onboarding workflows, credit decisions, and account servicing that customers never see but absolutely feel when they go wrong.

The most useful framework for understanding CX scope in finance is what practitioners call the 3 E’s: Engagement (are you reaching customers at the right moment?), Ease (how much effort do customers expend to get what they need?), and Emotion (how do customers feel after each interaction?). All three dimensions matter independently. A mortgage application can be technically easy yet emotionally cold, and that gap shows up in loyalty data within 12 months.

The critical distinction is this: customer service is reactive, marketing is promotional, but CX is the architecture that connects every function to the customer’s lived reality. CX has moved from a marketing function to a core economic discipline focused on long-term customer outcomes and trust.

How CX drives growth, loyalty, and compliance

The business case for investing in customer experience in finance is no longer theoretical. The data is specific enough to anchor executive decisions.

Growth is the most direct outcome. CX-optimized banks grow 3.2 times faster than competitors, with a one-point improvement on the Forrester CX Index translating to $123 million in incremental revenue for multichannel institutions. That number comes from reduced churn, increased product cross-sell, and higher average balances among satisfied customers. Loyalty, in other words, is not just a sentiment metric. It is a revenue lever.

The compliance dimension is less discussed but equally significant. Complaint volume trends are now recognized as a leading indicator of regulatory enforcement risk. Firms that eventually faced formal enforcement action showed sustained complaint growth averaging 24% year-over-year, compared to 12 to 18% for non-enforced peers. This means a well-functioning CX operation, specifically one that captures and routes complaint data systematically, functions as an early warning system for compliance exposure.

There is a direct connection between how you handle a customer’s frustration today and whether a regulator knocks on your door next year. Most institutions have not made that connection operational.

Pro Tip: Route all complaint data to a cross-functional review that includes compliance, CX, and operations leadership on a monthly cadence. Complaint patterns tell you where your processes are breaking, often months before the formal risk materializes.

The third dimension is personalization at scale. Embedding compliance into personalization engines allows institutions to deliver hyper-relevant customer experiences without violating regulatory constraints. Institutions that treat compliance as a design parameter rather than a filter applied at the end are the ones building genuinely differentiated CX. They are also the ones with lower enforcement exposure.

Common CX pitfalls in financial services

Most financial institutions are investing in CX improvements. Many of those investments are backfiring. Understanding where they go wrong is as important as knowing what to build.

“We implemented AI across our customer service channels to reduce costs, and our satisfaction scores dropped 11 points in two quarters. Customers were not looking for faster deflection. They were looking for someone who understood their problem.”

That quote reflects a pattern playing out across retail banking right now. AI used primarily for call deflection commoditizes the banking experience and erodes trust. The institutions winning with AI are using it to scale personalized advisory, not to reduce human contact indiscriminately.

Here are the four most damaging CX misconceptions in financial services today:

- AI is a cost tool, not a trust tool. Deploying AI primarily to reduce headcount signals to customers that efficiency matters more than their outcomes. The better application is AI that surfaces relevant product recommendations, flags account anomalies proactively, or personalizes financial guidance at scale.

- Channel handoffs are an IT problem. Channel handoffs are the primary trigger for poor CX and churn because customers are forced to repeat information when context does not transfer. This is fundamentally an organizational design and data architecture problem, not a technology ticket.

- Compliance is a constraint on good CX. This framing produces CX designs that get watered down at the legal review stage. Personalization strategies anchored in compliance consistently outperform those that treat regulation as a barrier.

- High complaint volumes are a service quality issue. They are a systemic failure signal. Credit bureaus and traditional banks with poor complaint management create reputational risks that official metrics rarely capture until the damage is done.

Recognizing these patterns in your own institution is the first step toward building a CX function that actually protects and grows the business.

Practical CX strategies for financial services executives

Knowing the problems is not enough. You need a clear set of decisions to make. Here is a practical framework that senior leaders in financial services can act on now.

-

Implement experience orchestration across channels. Every customer interaction needs context from the previous one. Invest in a unified customer data layer that transfers information seamlessly across digital, phone, and branch touchpoints. The goal is that a customer who starts a mortgage inquiry online and calls your contact center should never have to repeat themselves. This single change reduces churn and complaint volume simultaneously.

-

Build a Voice of the Customer program with compliance routing. Structured VoC programs that route complaint data to the right teams reduce escalation rates and surface regulatory risks early. This is not just a CX tool. Regulators increasingly view VoC infrastructure as a risk management asset. Your compliance team should have a direct seat in VoC governance.

-

Use AI to scale advice, not to deflect contacts. Identify the top 20% of customer interactions that require genuine expertise and use AI to assist your agents in those moments rather than to route customers away from them. This approach increases resolution quality and builds the kind of trust that retains customers through life events.

-

Integrate compliance checks directly into CX design. Use psychographic segmentation as a compliance-friendly alternative to demographic targeting. Psychographic segmentation allows nuanced personalization based on customer attitudes and behaviors without triggering the regulatory risk of demographic proxies.

-

Create a cross-functional CX governance structure. CX, compliance, operations, and product need to sit in the same room when experience decisions get made. Siloed ownership is why so many CX investments fail to produce measurable outcomes.

Pro Tip: When launching a new CX initiative, assign a compliance owner from day one rather than routing the finished design through legal review at the end. This cuts redesign cycles by an average of 40% and produces experiences that are both better for customers and safer for the institution.

Measuring and sustaining CX success

You cannot manage what you do not measure. But in financial services, the choice of metrics matters as much as the discipline of tracking them.

| Metric | What it measures | What it misses |

|---|---|---|

| Net Promoter Score (NPS) | Likelihood to recommend; directional loyalty signal | Does not capture specific friction points or compliance risk |

| Customer Effort Score (CES) | Ease of completing a task or resolving an issue | Does not reflect emotional dimensions of the relationship |

| Complaint volume trends | Systemic process failures and early regulatory risk signals | Does not always capture silent churn from disengaged customers |

| First contact resolution (FCR) | Operational efficiency in handling issues | Can be gamed if resolutions are logged but not genuinely complete |

The relationship between these metrics matters more than any single score. NPS works best alongside complaint data and operational KPIs, and the direction of change over time is more important than the score itself. A high NPS that is declining tells a different story than a modest NPS that is steadily improving.

First-contact resolution in call centers correlates directly with customer satisfaction and lower overall complaint volumes. Institutions that consistently resolve issues in a single interaction build a reputation that is harder to damage and more valuable to protect. Measuring FCR alongside CES gives you a fuller picture of where your processes are breaking down and where they are working.

The goal is to align your CX measurement framework with financial outcomes and compliance milestones, not just satisfaction benchmarks. When you can show that a five-point improvement in CES reduced complaint escalations by 18% and saved a measurable amount in compliance remediation costs, CX stops being a cost center in the executive conversation.

What I’ve learned about CX in financial services after years in the field

I’ve watched financial institutions spend significant budget on CX transformation programs that produced glossy reports and almost no behavioral change. In my experience, the failure point is almost always the same: executives treat CX as a project rather than an operating model.

The currency of financial services is trust. Not rate. Not product. Trust. A single poor experience during a sensitive moment, such as a disputed charge, a loan denial, or a fraud alert, can undo years of positive interactions. I’ve seen this play out repeatedly, and the institutions that recover fastest are the ones that have built CX infrastructure that treats those moments as high-stakes operational events rather than service calls.

What I believe most strongly is that compliance and personalization are not opposites. The best CX work I’ve seen in this sector embeds both from the start. The teams that separate them always end up with one watering down the other.

The operational detail that keeps me up at night? Channel handoffs. It is the single most underestimated driver of churn and regulatory complaints in banking. Fixing it requires organizational will more than technology budget.

A mature Voice of the Customer program is the most underutilized asset in most financial institutions. It is simultaneously a CX improvement engine and a regulatory risk radar. If you have one and compliance does not use it, you are leaving half its value on the table.

— Daniela

How Altiamcx helps financial services organizations build better CX

Altiamcx partners with financial services organizations to close the gap between CX strategy and operational execution. From customer care and complaint management to back-office support and team extension, Altiamcx brings the cultural alignment and performance discipline that financial institutions need to deliver consistent, compliant experiences at scale.

Whether you are building a cross-channel resolution capability or scaling a VoC program that supports both customer outcomes and compliance goals, Altiamcx provides the infrastructure and expertise to get there without the overhead of building it entirely in-house. See how a nearshore team extension model can accelerate your CX roadmap while maintaining the quality standards your customers and regulators expect. You can also explore how Altiamcx has helped organizations achieve productivity improvements of up to 89% by restructuring support operations around the customer, not the process.

FAQ

What is the role of CX in financial services?

CX in financial services covers every customer interaction across digital, branch, and contact center channels, functioning as a driver of loyalty, revenue growth, and compliance risk management when managed strategically.

How does CX affect financial institution growth?

Banks with optimized CX grow 3.2 times faster than competitors and generate $123 million in incremental revenue per one-point CX Index improvement, making it a direct contributor to top-line performance.

Why is customer experience important in banking compliance?

Complaint volume trends predict regulatory enforcement risk, with enforced firms showing sustained complaint growth significantly above non-enforced peers. A structured CX operation gives compliance teams an early warning system built into normal business operations.

What CX metrics matter most for financial services executives?

NPS, Customer Effort Score, first-contact resolution rates, and complaint volume trends work best as a combined framework. Trend direction matters more than isolated scores, and all metrics should tie back to financial and compliance outcomes.

How should AI be used to improve customer experience in finance?

AI delivers the most CX value when used to scale personalized advisory and assist agents in complex interactions, rather than primarily reducing human contact. Institutions that balance AI with human empathy consistently outperform those deploying it purely as a cost-reduction tool.